Final Tax Bite

This calculator estimates your estate's tax liability at death with no surviving partner.| Alberta |

| Regular taxable income in year of death |

50,000

|

| Estate Assets | |

| These are considered to have been sold for fair market value immediately prior to death. | |

|

Registered Assets

Registered Assets

The fair market value of RRSPs, RRIFs and DPSPs is included your income in the year of death and is taxed at your regular personal income tax rates. |

Market Value |

Original Cost |

Capital Gain |

Taxable Amount |

| RRSPs |

100,000

|

N/A

|

N/A

|

$0

|

| RRIFs |

0

|

N/A

|

N/A

|

$0

|

| DPSPs |

0

|

N/A

|

N/A

|

$0

|

| Total registered |

$0

|

N/A

|

N/A

|

$0

|

|

Non-Registered Assets

Non-Registered Assets

Non-registered assets are considered to have been sold for fair market value immediately prior to death. Any resulting capital gains are 50% taxable and added to all other income your final return where income tax is calculated at your regular personal income tax rates. |

||||

| Mutual funds |

0

|

0

|

$8,000

|

$4,000

|

| Stocks, bonds |

0

|

0

|

$8,000

|

$4,000

|

| Real estate |

0

|

0

|

$8,000

|

$4,000

|

| Vacation property |

0

|

0

|

$8,000

|

$4,000

|

| Business |

0

|

0

|

$8,000

|

$4,000

|

| Other |

0

|

0

|

$8,000

|

$4,000

|

| Other |

0

|

0

|

$8,000

|

$4,000

|

| Total non-registered |

$0

|

$0

|

$0

|

$0

|

| Grand Total |

$370,000

|

$328,000

|

||

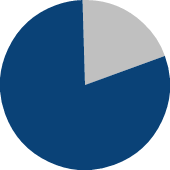

Taxes on Your Estate

| Pay taxes of: | $29,551 | 8.0% | |

| Estate keeps: | $340,449 | 92.0% | |

| Total estate: | $370,000 | 100.0% |

Assumptions

This calculator is for illustration purposes only and is not intended to calculate your actual tax liability. It provides an estimate of the tax liabilities at death assuming there is no surviving spouse.

Calculations use marginal tax rates as of . Rates take all federal and provincial taxes and surtaxes into account and the basic personal tax credit. The capital gains inclusion rate is 50.00% on capital gains up to $250,000 and 66.67% on capital gains above $250,000.

Only Canadian assets are included in the calculations. The tax on your estate is the difference between the tax payable on your regular income (before any deemed dispositions of your estate's assets) and the tax payable on your regular income plus the taxable amount of your estate.

Disclaimer

This calculator is for illustration purposes only and is not intended to calculate your actual tax liability. It provides an estimate of the tax liabilities at death assuming there is no surviving spouse.

Calculations use marginal tax rates as of . Rates take all federal and provincial taxes and surtaxes into account and the basic personal tax credit. The capital gains inclusion rate is 50.00% on capital gains up to $250,000 and 66.67% on capital gains above $250,000.

| Capital Gain | Inclusion Rate | Taxable Gain | |

| First $250,000 | 50.00% | ||

| Above $250,000 | 66.67% | ||

| Total |

Only Canadian assets are included in the calculations. The tax on your estate is the difference between the tax payable on your regular income (before any deemed dispositions of your estate's assets) and the tax payable on your regular income plus the taxable amount of your estate.

| Taxable Amt | Tax | ||

| Regular + estate income | A | $378,000 | $147,451 |

| Regular income | B | $50,000 | $8,883 |

| Estate income | A-B | $328,000 | $138,658 |

Disclaimer